Office Hours: What’s New in Home Consumer Engagement

Industry, Strategy

| 27 Aug 2025

Summary

A few weeks ago, Local Logic’s Head of Corporate Strategy and Business Development Sara Maffey joined Nathan Brannen, Chief Product Officer at Restb.ai, for a masterclass moderated by Brian Bell, PropTech Innovation Practice Lead at Accenture.

For close to an hour, they discussed:

Sara Maffey (SM): I’m Sara Maffey, the Head of Corporate Strategy and business development at Local Logic. Before joining Local Logic, I worked in commercial real estate. Local Logic quantifies everything outside the four walls of the asset for every asset in the U.S. and Canada.

Nathan Brannen (NB): My name is Nathan Brannen, and I’m the Chief Product Officer at Restb.ai. For the past ten years, my background has been in AI and looking at how it can create new opportunities and help people make better decisions, which led me to Restb about four years ago.

At Restb, we focus on the visual insights you can gain by looking at a photo. And if we think about the U.S., where there are over a million property photos uploaded every day, there are a lot of hidden insights that are there for the taking.

Brian Bell (BB): I spent a lot of time working with automation, valuation models, data, and appraisals. I’m pleased to be able to host this today and move us forward. I’m excited about how locational and photo-based data change the game, including in property and casualty.

What kind of data and insights can you drive with photo-based AI, and what is it?

NB: When we talk about photo-based A.I., some people call it image recognition. But you can think of it as how AI understands what’s within an image. So when you look at a photo, you’re able to understand a lot about what’s in that photo, and you can train AI to do that.

So this can be simple things like we’re looking at a kitchen and we’re looking at a living room. So you can talk about the features that are present within a photo, and you can even do more complex things like understanding what is the style of a home, what is its quality, what is its condition, how can we score these things across our standard scale to generate datasets that you can make decisions on?

And all of this is built based on a lot of training that you put together to have the models work and how you want them to work. And that gets quite interesting because, with real estate, it’s pretty specific to where you’re located. So Miami is very different than, say, Boston or New Mexico. And that’s just within the US. So we can get a lot crazier as you go further away in different countries.

And so we spent a lot of time trying to understand the data points that people need that come out of these photos. And then, we work to train and create various standardized models that can be used at scale for people in the real estate vertical.

BB: You mean to tell me if I go on Pinterest today, I can pick my favorite kitchen, I can upload it into the database, and you would be able to find identical matches?

NB: I don’t know about identical matches, but very close. Using that same process, you’d be able to, you know, use a lot of the abstract look and feel of photos. You can find other properties or pictures that are very similar.

BB: So, from a real estate perspective, this changes because you’re no longer using data points in your search. You’re using images in your search.

NB: I think it’s a data point, it is an image, but I think it’s just a natural way of people interacting with real estate. A lot of what we do with AI is trying to take processes that exist today and make them a lot simpler. So if you’re someone who’s looking at a home, you may visit a bunch of other homes trying to find something that looks similar to the house that you like or maybe your past home or your dream home. But you’re doing that inefficiently by going to every home in person or scrolling through all the photos. So what we want to do with AI is say, hey, we can look through these millions of photos all at once, and we can return you what you’re looking for based on similarities, specific features, whatever it may be.

BB: So similarities can help the appraiser in their selection of comparables, realtors in the selection of comparables, and possibly the end consumer around similar-looking properties.

NB: Absolutely. I think that’s one of the areas that we see a lot. And, you know, we talked to different people in the investment space and in other areas, and one of the challenges they have is the manual effort it takes to truly review a property, Say you have a team looking at 100 properties a week. That’s great. Maybe five of those properties meet the criteria; they’re valid comps. But imagine if you could scan an entire market of 10,000 properties and return them the ones that the AI says are the most likely to be relevant for, say, a buy-box or whatever it may be. And then you can have that human team analyze those same hundred properties but find 50 that are good fits rather than just five.

BB: Now, let’s bring in Sara to give us some insights into the locational attributes related to the property because property valuation is predicated a lot on what is surrounding the home, and it’s one of the key features around it. So, Sara, give us your perspective around, you know, the data and the insights that Local Logic can provide.

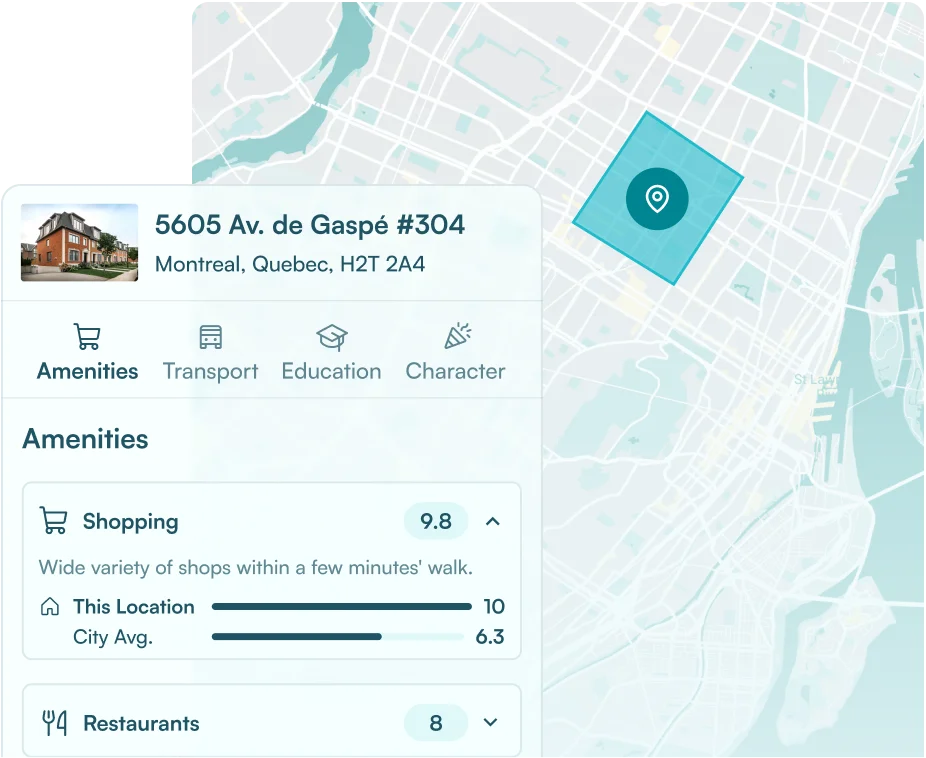

SM: Absolutely. Our models show that about 50% of the value of a property is based on location and not just what’s inside the four walls itself. And I like what Nathan started with, of using data to quantify the human experience because I think we’re doing that outside the four walls of the asset.

Our location scores are the backbone of our products. We objectively understand things like access to transportation parks, greenery, retail, restaurants, and what you think of as being more subjective, like vibrancy, quiet, and our new wellness score. So we’re covering the full gamut of what you would experience boots on the ground on the site. But we’re allowing folks to understand that through data so they don’t have to visit every site. I think this is really important, as we’ve seen many investors looking in new markets where they might not be as familiar, or as Nathan was saying earlier about looking at portfolios or opportunities at scale. So I think it’s imperative to start using data for that

BB: It’s amazing. Tell me a little bit more about your wellness score. That’s the first I’ve heard of it. I want to be “more well”, and how does that relate back to my home or the “location, location, location.”

SM: Yes, I love it. Well, we just announced it, and it’s really focusing on access to healthy behaviors and healthy food, things like that. So are you near yoga studios, gyms, that type of thing, or do you have access to parks, run, walk kind of paths and trails? I think the Atlanta Beltline because I’m based here in Atlanta, is a perfect example of that. And then just healthy food options. I think a lot of times, understanding that you’re going to have access to those healthier grocery stores, farmer’s markets, things like that.

BB: How have you seen the real estate in the valuation industries change due to the pandemic and what transformational changes have you seen occur?

NB: It’s been a pretty crazy couple of years. And I think some trends were already happening before the pandemic started that have been accelerated quite a lot by what’s happened with the pandemic. So if you look at something like an iBuyer, this concept existed before the pandemic happened, but it became more front and center over the past couple of years, and I think a lot of that also applies to, say, institutional investors.

You see a lot more activity there in different markets. You see anywhere from one in four to one in five homes that are being bought by institutional investors. And this can be from things like the lower interest rates that have happened. But the impact of this on the iBuyers is creating a new paradigm within real estate, particularly in the valuation space.

According to Redfin, in 2020, most homebuyers put in an offer without ever seeing the home they were purchasing. And that can be related to the fact that you know, homes are not sitting in the market as long, you know, prices are appreciating so quickly. And there are a lot of different factors that go into that.

But the impact of that is you need to be able to make decisions more quickly. So, for example, suppose you’re making investment decisions. You need to manage your risks so you don’t end up like Zillow and quite underwater in the amount of money you’ve deployed. So I think both Local Logic and Restb try to generate this actionable, consumable data that can aid in this changing world of real estate and particularly investment vertical.

BB: When you see these overheated markets, I guess the demand for data and insights becomes more important than ever.

SM: I think it does. I mean, things are moving so quickly, and you’ve seen investors even start to look at asset types that they weren’t investing in previously. They’re really starting to expand. And so, when those opportunities come up, you need to be able to move quickly. And using data is a really great way to assess opportunities more efficiently.

BB: I would agree that, you know, at Accenture, we’ve been beta testing the Oculus and the virtual reality software. Do you really see that? And I’ve been beta testing it in meetings and various aspects. And the first sort of thought that came to mind was, oh my gosh; this would really apply in real estate. So how could you not do the walk-through now through that, are you guys seeing your data and your solutions playing a role in that as we move down to the future?

SM: I think that that kind of mirrors, even the virtual touring, has really taken off, especially on the commercial side over the last couple of years, where that was obviously happening prior to the pandemic. But I think that it speaks to the industry’s increased comfort level in using data. And for me, that’s an excellent thing because I think before the pandemic, folks were kind of trying to dip a toe into it. They weren’t quite sure. But I’ve seen even in the last six months that so many firms have started developing their own platforms or the ability to use APIs, and that’s just going to increase.

NB: I think it’s really just part of this trend of greater adoption of technology, greater leveraging of technology. You’re seeing a lot of new entrants. A lot of this money comes into the space that’s having people push more aggressively on these new ideas and these new ways of doing things than they have in the past.

And you combine that with millennials becoming one of the larger home buyers or segments, and all of these things just are contributing to quite a fast change. So I think the past two years, we’ve seen greater change than maybe the past two decades in some ways, with just the change in how things are done in the amount of this innovation and new ideas coming into this world.

BB: When we look at the real estate market, we tend to look at you as the consumers. And when we’re talking single-family residential, you have the consumer segment that is buying. You’ve had the real estate investor segment. And I think a big one that we’ve seen now is that the institutional / pension companies are starting to look and get into the residential segments. And do you think that’s going to change the real estate market dramatically? With these well-capitalized institutions being able to drive change?

NB: I think it’s going to change things. I am split on whether all those changes are necessarily good for the average home buyer. But the reality is whether you’re a fan of it or not as if that is happening. Some funds are deploying incredible amounts of capital to purchase properties and spend a lot of money acquiring data to make the best decisions on these properties.

And you’re seeing a lot of regional players who are comfortable maybe investing in the metro Atlanta market. And, you know, they’re good at understanding what worked there and what didn’t work there. And they’re going, man, I’m doing great with this $50 million fund, but someone wants to give me a half-billion dollars and I can’t find those properties in Atlanta. So how do I spend out, and how do I do that with the same success I’m having in my backyard or my home market? And, you know, real estate changes so much as you move to different markets.

So I think you’re going to see some cases like with Zillow where maybe it isn’t as simple as it seems, but what we want to help is provide data for both those companies to make better decisions, but also the individuals and the agents to help their homebuyers make better decisions as well.

SM: I think we can understand markets from both the consumer and analytics side of our products. Maybe start in Atlanta because that’s where you’re comfortable and begin to understand with our heatmaps and location scores how that area matches based on those different factors. And then you can take that anywhere in the U.S. and Canada and look for similar areas.

One of my favorite parts about our location scores is how we show at different scales. So we’re showing a score at the actual site itself, the neighborhood, and the city. So you might think, oh, you know, this seems like a great area for walkability, but then you get that context of understanding how it fits within the market itself, and I think that’s really helpful as you’re trying to expand into new geographies.

BB: One of the questions that always comes to mind, and I’m also a real estate broker, I’m licensed, and it’s you we question a lot at Accenture is the role of the realtor and how they’re impacted by data and technology?

SM: I think that what we’ve seen over the last couple of years is, as Nathan alluded to earlier, that folks are doing a lot of their research before they even reach out to a realtor or broker. And so having our data on a site so that you can do your own research and understand the context of different neighborhoods or cities before you even speak to someone, I think that really helps.

We’re also adding stickiness to sites and giving a lot more context to actual listings. So that has really helped quite a bit.

NB: I think it’s not meant to replace the realtor. There are many things that AI can do, and there are many things that AI can’t. And so if you’re a home buyer searching on a portal, you’re thrown so much information, a wellness score is great, a noise score is great. And like, all these things are very valuable. But it can be an overload for someone who’s buying a home for the first time or buying a home for the second time. But it’s been 20 years since they bought their last home. And the realtor’s job is really to understand how that information sits within its market.

So I love what Local Logic is doing there. We’re looking to do very similar things and say that this home is lovely. It could even be the nicest home in this neighborhood. But that’s different in that particular zip code is actually at the bottom end of that spectrum and the quality of that home. So all this is a crucial context to help someone determine where they want to live next.

But it’s beneficial to have a realtor who has all this insight and experience to help guide them through the implications of that particular purchase based on what they’re seeing. And I know that is something that will continue. And what we’re doing is providing data to make that easier for the realtor, so they don’t have to drive through a neighborhood to get a feel for what that area’s noise score is. They can have that insight and then be able to translate it into words that homebuyers will be able to relate to.

SM: That mirrors the ability to put that information in the homebuyer’s hands or the renter’s hands. Our one-click reports make that easy for the realtor too to get all of that information in less than a minute.

BB: I think it really enhances the role of the realtor because now they help the client understand and learn all of this new information. There’s more information than ever. And I think it’s a great opportunity for the realtor to showcase their knowledge and expertise by leveraging those insights and the data.

And we see that photo-based A.I. helps with architectural styles and visualization. So the clients may be looking at fewer homes, but the role of the realtor has actually become more important than ever with understanding these insights.

As we start to look at, you know, the marketplace, how does your data really help with looking at real estate opportunities and the assessment of these opportunities in terms of location, risk assessment, and looking across a vast geography? How do you empower somebody like me to say, okay, what about the Atlanta market or other markets?

SM: I think it’s about understanding what’s important to you from the get-go. Like, what are you looking for from a quality of life standpoint? But also on the risk side. So we also have partnered with ClimateCheck. So if climate risk is important to you to consider for the long term, that’s data that we’re making available via our MLS partnerships and on our own platform so realtors can have access to that as well.

But I think understanding how neighborhoods will change over time is another significant factor, and that’s on our roadmap. So we’ve been collecting data for over six years now on all of our location scores, and we understand how neighborhoods have changed. We’re working to put that information, and those insights in the hands of our users so they can start to understand the risk of location in the future as well.

It’s a major investment, whether it’s a commercial asset or a home. And so you want to understand what that ROI is going to be, whatever your hold period is going to be.

BB: Would you look at the locational data from a macro perspective? You can zero in on the key things that are important to bring you one to you. Maybe a concentric circle closer to where you’re getting to that. What do you think of this?

SM: Our solutions are really flexible, so you can start by understanding them at the market level. I think it’s fascinating. We’ve seen on the consumer-facing side that using our heat maps; for example, folks actually start to look about 50% further out than they were initially even considering because they begin to see areas that match the lifestyle that they were looking for, maybe a little bit beyond where they originally thought they were going be able to find it so I think that that’s one way that we can add value.

BB: I think it makes sense to understand how you move from a macro to break down to the location. When we look at real estate boards, I’m a huge fan of the U.S. In Canada, we’re a locked market, so brokers and consumers have very little access to this data, which seems to be a miss. I’m amazed how Local Logic and Restb are working with these real estate boards to really advance the industry to the next level, which I think Canada has been missing. And we’re very envious sitting from our side.

NB: I think us coming in as a company that was more of a technical company, more an AI company with our experience and understanding how to extract these insights, that image we’ve had to learn a lot about the landscape of real estate and, and how that works with the different boards, with the associations, with who has access to what and who can do what. And it’s been interesting navigating that. I think there’s been a lot more reception to the type of things that we’re doing over the years. And the idea that all this can be great for the agents, for the consumers who are buying and selling homes, and that it’s one of those things that I think that we hear: what you guys do just makes so much sense. Everyone will be doing that in three years, five years.

And I think if you have that mindset, then it becomes, all right, well, why are we not doing it now? What are we waiting for? If it makes sense to improve this entire real estate process and we’re starting, I think we will see a lot more acceptance of that and adoption. And now we’re even getting those conversations where, you know, the people we’re speaking with are thinking bigger than even we’re thinking. We’re like, oh, wow, that’s a great idea, let’s go take that back and see what we can do.

BB: I think we’re going to start to move a little more around, you know, talking about valuation models and maybe giving us some insights around the challenges that investors encounter when building their automated valuation models.

And we’ve seen Zillow. Zillow has been around for a long time; I’m a big advocate because there are no Zillow equivalents around real estate in Canada. Regarding valuation models, what are the challenges you’re seeing with companies in the U.S. or around the globe with building their valuation models today?

SM: I think it’s really hard to get objective location data. We’re often seeing that our users are used to relying on their own personal experience in a market or maybe their brokers’ experience in a market. And yes, there are things like Walkscore, but they’re only covering a specific portion of the experience in our algorithms.

I think it’s worth noting that we were founded by urban planners. So really, at our roots, we understand what makes neighborhoods livable and what makes cities match the quality of life that folks are looking for. And what I think is really cool is being able to go from the city level down to that specific site. So we’re really bringing you to the front door where Nathan takes over. We’re working with MLS, and we’re also working on the commercial side. So it’s just an objective way of actually understanding the whole ecosystem that you’re experiencing as a human in a place.

BB: So generating a value on a property is not complicated. In our consulting practice, we’ve helped many people generate the value. Generating a really accurate value, I would say, is complicated. So when you look at property valuation and you come up with the value, do you think that the new AVM models are going to start to look like appraisers, where they make deductions based on climate score, locational scores, maybe positive attributes or negative attributes based on locations like are you seeing the trend in the industry where companies are looking at it from that perspective, like that appraiser mindset?

SM: I think people were doing that to some extent before, but they weren’t acknowledging it because they were doing it more subjectively. But absolutely. I think that that’s absolutely the direction we’re going in. The other thing I would add to that is also understanding how those things are going to change over time. So you might understand it today. And I think that that’s the snapshot you have. But that’s why our predictive scoring will be such a game-changer because that’s what will drive your ROI over time is how that neighborhood’s going to change around you.

BB: At Accenture, we do a lot of consulting with the government and many large companies. And one I’ve been personally working on is climate change. It has such a significant social impact around the scoring because if today you identify a house. You say, well, this has a high flood potential now that it didn’t, so that could cause maybe the homeowner to not get property and casualty insurance or the mortgage not renewed. So many social issues come with the data now that we hadn’t thought of. And how do you think we’re going to be able to handle or navigate through these things?

And, you know, it’s a tricky question, and you probably don’t have the answer, but I just think it’s awesome that the data is going to show it is going to create a new problem called “What do we do now?” So if you identify my houses in the floodplain or fire risk, you know, it’s good to know. And maybe it’s the education factor. That’s the solution. Is that where you see the power of your data is around education?

SM: I think it is part of that. I mean, it’s really empowering people, whether they’re an investor or homebuyer, to understand that risk at the very beginning. It brings up questions about whether we should be building in some high-risk regions. I know just in my past life, working in disaster recovery, that came up over and over again as you had to rebuild in flood zones. And so I think that it brings up all sorts of social issues. I believe there are other cool things that our data can help with on that side as well in just identifying areas of opportunity, like, hey, you know, a mixed-use developer of this area could really use access to a grocery store or empowering cities to understand where their services are needed with rapid transit or parks and things like that, so I think there’s a lot of like social equity that comes from our data as well, which is really exciting.

BB: Yeah, social data models are on the rise. Like we’ve been working with the government around affordable housing and how do you use predictive models around how do we, you know, how do you put vulnerable groups, and a lot of it is locational data that we’re using today.

How about the inside of the buildings? So we know the locational data is used to maybe adjust up or down a property value. What are the challenges you’re seeing on the interior of the property or even the physical exterior of the building?

NB: Yeah, it’s interesting hearing a lot of what Sara said, just because there are so many parallels to what we’re seeing with what we’re doing within that property are looking at that property on its own.

And one of the big things that we run into looking at the data is that it’s so important that the way you’re collecting data is standardized across the country. And even with things that are in the tax record, you know, we have AVM or valuation clients who say, yeah, we know that half of the counties have terrible data for these data points, but you see it in there, and so you assume it’s correct.

But then when you look at the scores that, say, Local Logic provides or that we provide, there’s a lot of you know, hey, what if it’s wrong? What if it’s not right? So you do want to be cautious with these things. But I also think you want to be aware of, you know, what is the actual risk and, you know, where it may be acceptable to use.

And so I’ll give some examples. With AVMs, we know there’s not a non-trivial amount of AVMs that are scanning the listing text or the listing remarks to pull out, you know, words they may identify. Right. Is it a fix and flip opportunity? Is it more luxurious? And if you think about having, what is it, 1.5 million agents in the US all marketing their properties in different ways and then trying to take out that text to then apply a condition score that’s a component within your AVM. So I think what we’re doing becomes a lot less scary by providing a standardized model that works across all these properties.

On the flip side, with something like an appraisal and some of these more regulatory areas, I completely understand you not wanting to get your loan denied because of what a computer said. However, there’s still an opportunity there at the same time because, you know, if you were someone who had your home appraised and they said that it was in disrepair. Our models said that it was not in disrepair at all, it’s actually in quite good shape; you’d want that to be flagged through our quality control process.

And you’re able to 1,000 x, 10,000 x the amount of quality control you can do by looking to see where there are the big deviations between what an AI model says and what was recorded and appraised.

And you can also start getting into things like bias and some of the things that have been in the news recently. I think Fannie Mae just released a 50 plus page report about trying to eliminate a lot of the bias disproportionately affecting certain minority groups. And I think that AI and the standardization and this broader look at scale of how we do things can really help, you know, lead to better decisions, lead to better processes and help the industry overall.

BB: So in terms of looking at a photo or you’re you mentioned earlier, Nathan, you’re able to give it a score. So would that be a score based on quality? So an appraiser in the U.S. would have a condition score between one and six. Are you saying that the technology today would be able to give you a similar scoring to an appraisal methodology?

NB: Correct. So when we first started, we were starting more in the AVM investor space. And for this, we had an all-encompassing score that looked at the quality of the property, the condition, the potential. You know, if I put $100,000 into this property, am I more likely to get $120,000 out, or am I more likely to get, you know, $250,000 out, a lot of things that, you know, look at the property and in the case of potential, also look at the surrounding area.

But as we started moving into the different use cases, different people have different requirements. So the appraisal world is a great one because Fannie Mae says, hey, you need to describe a property on its condition from C1 to C6, and you need to describe it as quality from Q1 to Q6.

So, you know, to work in that space, we really need to match the existing standards. So now we have a C1, C6 model that maps that, you know, as perfect as we are able to get for their scores, and we’re working on a quality model to match that use case.

But even if you look at another industry like the rental space, the way that condition works in, say, rentals is a little bit different because, you know, if you’re renting a property out it’s more about all right, I, I want a property that I don’t have to do any work to be able to rent out if I’m an SFR investor.

So the way we would want a score that would be slightly different than if we’re looking at a property that someone’s going to move into and live in because they may be more worried about “All right, what are the things near the end of their life that I’m going to have to upgrade or I’m more likely to upgrade based on where this home is in this particular market,” kind of the expectations of what someone living in that house would do potentially have? And so I just see us going deeper and deeper and more granular and granular as we start to understand the different use cases of these different players.

But the score itself and I think Local Logic has done such a great job with these scores. They’re so important because it’s so much easier to consume that score than it is to consume, you know, three-quarters of the home had carpet, which was about ten years old. And, you know, all the other homes in this neighborhood and hardwood floor is like that.

That’s the process we need to solve to make it easy to make decisions on this type of data.

SM: And I think just adding to that, like you’re talking about all these different use cases of the home, like whether it’s, you know, SFR or short term rental or the someone’s actual primary home. And that’s one of the reasons I really like the ecosystem of scores that we have because it is about understanding the persona of who’s going to be using that space and what they’re looking for. And on our end, you know, what they’re looking for and the location of that home. And that’s why, you know, we now have almost 18 scores when we add wellness. And so people can really use whatever scores make the most sense for what they’re looking for.

So people will often run a regression on their past portfolio to understand which of our scores are actually correlated the most with creating the value that they’re looking to create out of that asset. And that’s just one way to start using that objective look at location to create value.

BB: So when you look at the real estate process, you buy the home, and then the appraiser has to go in value on behalf of the mortgage company. So based on what I’ve heard between Local Logic and now with Restb, it looks like the appraisers’ role could change dramatically now that they maybe don’t even need to go to the property anymore. Do you think that’s a trend that could realistically take place?

SM: Absolutely. I think Clear Capital just posted a really interesting article on desktop valuations. And I think especially over the last few years, as we’ve talked about, so much has been happening virtually. And if you can understand the neighborhood around a site virtually, then why not do that? But, at least as a first pass, especially if you’re looking in SFR when you have these massive portfolios of scattered sites, you basically have to do that to be efficient. Otherwise, it will take way too much time to do that manually and in person.

BB: Makes sense. I led an appraisal management division, and appraisers getting bit by dogs is more common than you actually think. So appraisers would probably be glad to be staying at home and doing more desktops and comparative assessments.

NB: I think it was last week that some new regulation came in from Fannie saying that I think up to 20% of homes are now eligible for a desktop appraisal. And as I understand it, that’s related to the increased need for appraisers with three phases with more home purchases.

The appraisers themselves are an industry that is not getting younger. It’s one that there’s not a ton of people moving into. So how can we make each of those appraisers and all their, you know, careers of experience be more efficient, and so if you can save an hour trip both ways to a home and allow someone to do that via a desktop using the technology and tools that are now available, I think you can get a lot more value out of each of those appraisers and make this whole system work more efficiently.

At the same time, I want to stress that I don’t think we can replace them today and I don’t think, you know, in five years we can completely replace what’s being done with an appraiser and where they sit with, you know, valuing the collateral you have in a loan. But we can certainly make their jobs a lot easier, we can certainly make them more consistent, and we can certainly help flag areas where, you know, that mark has been missed, which is quite relevant.

And, you know, I was speaking with someone in Toronto and with, you know, the appreciation in home prices now, the appraiser’s job is kind of impossible. So how do you get to the number that you need to get to for what that house was so that it’s very hard based on kind of the way that property worked 12 months ago or six months ago.

And so as you start having these markets moving so quickly, as you have to look at comparables where the prices may be so out of whack with what you know would have been the case even three months ago, how can we help figure out what to do and what to make sense and not to have a huge systemic risk put into the system? You know, that’s bad for everyone.

BB: With an aging demographic around appraisers, how do we make this segment much more efficient and improve how they can do it? And speed, improving their overall transaction time, which I think is a really important thing.

So if we put things into perspective, if you’re a realtor today or running a brokerage, you’re quite excited about what locational data can do when combined with Restb being photo-based artificial intelligence. If you’re an appraiser today, you’re viewing the new tech in this disruption, not as a big change to my business, but as actually making me more efficient and moving forward as both of you tend to look forward in the industry.

Like what are other exciting things you’re seeing in the marketplace that would be helpful to maybe our audience to see what’s coming down the pike you’re both innovators. You’re both on the leading edge. What else is coming that that should be really exciting when we look at it.

SM: I think I’ve mentioned it before, but what I’m really excited about is on our roadmap of being able to predict how neighborhoods are going to change. I think that that’s going to be the biggest game-changer, you know, being able to really understand how maybe one change in the neighborhood is going to be the catalyst that makes all the values go up.

So I think that that’s going to be a really important addition that we’ll be adding. The other piece of it is sustainability. I mean, we kind of touched on social equity before, but I think from the investor side, and from the consumer side, people want to understand their environmental and social impacts and they’re starting to actually consider that in their home buying choices and certainly from institutional investors ESG reporting is just becoming, you know, required at this point. A lot of the frameworks for that are still sort of working themselves out, and we’re really focusing on GRESB as sort of our framework that we’re using, where we approach sustainability looking to understand projects, impact on the community, the livability, the access to transportation.

And we have scores for all of those things. So I think just being able to package that and make it more automated for folks to understand the environmental and social impacts of location choices, it’s going to be really important right now.

NB: A lot of what we do now is inside the four walls of our home but how can we take what we know about the inside of the fourth walls for an entire market and provide those insights, you know, as a snapshot in time as well as, you know, the trends that we’re looking at.

And as an example, there are let’s say we know that in a particular zip code, there are three modern homes that are sold every month. I’m now a realtor working with my client and they really are dead set on a modern home in this particular market. Rather than updating, you know, Zillow every day and seeing what’s there. It’s a lot better if you can say, hey, you know, right now what you want isn’t really available. There’s going to be higher demand for it because it’s below what it should be.

What if we were actually to look at other properties that could be converted into what you want and completely reframe that discussion very early on in that process with respect to what decision that person is going to make and what that would look like. And I think these types of decisions are able to be made easier when you have this type of data, when you have that snapshot.

Another example would be, say you’re a new developer and Inman.com is telling you, hey, you know, white kitchens are out or white kitchens are in or whatever it may be, that’s all helpful. But that doesn’t really apply across every market in the U.S. So we can give that type of insight of saying, hey, you know, here’s what has been trending up over the past 12 months with regards to what people like you know, this is what you need to build because it’s what the market’s asking for.

You can basically drive these efficiencies that are maybe not that big of a deal in the big scheme of things. But, you know, to each of these businesses, each of these, you know, decision-makers in these processes, these are all relevant and things that they’re doing on, you know, maybe gut feel or a hunch that isn’t going to be as reliable as something backed by data over the long term.

BB: So now that you’ve both really educated our audience around the importance of locational data, the importance of property data specifically, and photos on the inside and the outside, I think a big question, and I see it a lot in our consulting practice with our clients is like the okay, so what’s next? You know, what do I do and how should I put all of this information in context?

And I think the right way to look at it when you’re talking about property, locational, and, and about unique properties is one you have to determine in your business. One, how important is property data to your business. And if it’s a core competency to your business and is something that that strategic investment you should be looking to make because that causes disruption in a lot of markets if you’re not investing into there.

So from an outside consultant perspective that’s a really key piece. How important is it to your business and will your business be disrupted if you’re actually not making investments into these future technologies and changes and advancements?

NB: One quick thing on what you just said that we try to explain, we’re speaking with people with these types of technology. It’s not like, you know, we’re giving you something that you had before. But it’s better. Oftentimes, what we’re providing to you is an insight that was invisible before. You can’t have someone go look at every home in the market constantly to understand the state of that market. But with something like computer vision, that’s not impossible.

There are similar things with the location analytics that are provided by Local Logic. With this new type of data, it’s not the same as having these existing property datasets that people have been working with for the past 20 years. No, this is a completely new dataset that has completely new implications.

We’re seeing it move the needle with, say, valuations in a way that is very meaningful, such that really nobody wants to talk about what they’re doing with it because of the competitive advantage they think it gives them. And so I think you have to start thinking, all right, you know, this isn’t what we’ve been planning for the past five years because we didn’t know that this was going to be possible at this point.

So instead, what are the implications of, all right, I can send or I can get the insights on every property in the market as if I were walking through them. What does that change with my business model? And that’s going to be different for each player that fits in the real estate vertical. But you have to be asking yourself that question and the other questions around these new innovations within this industry because it will fundamentally change your business model, what your future looks like and where you need to be investing now because it’s going to be too late if you wait a year or two.

BB: You need your property data and locational data as the game-changer. And this is going to be the game-changer in the real estate vertical. It’s going to be the game-changer in the appraisal and the valuation and it’s even going to trickle in the property and casualty. So it’s amazing how much investment is being made around property data today and driving that core differentiator in the marketplace.

SM: I think you’re pointing out really the risk of not using data. I think it’s you know, on our consumer-facing side, we have about 90% market share on home search sites in Canada. We’re growing in the U.S. So it’s kind of like you’re almost too late. Like you need to get on board with this. And, you know, we’ve talked about all the different values of using location intelligence on the commercial side. But I think we’re getting to a place where data is not just a nice to have you have to use data to actually compete in the market today.