New Search Filter Brings Large Geography Support to Lifestyle Reports

Product

| 10 Mar 2026

Mortgage teams heavily invest in competing for borrowers once rate shopping begins, but our data shows that by that point, many borrower decisions are already taking shape.

After analyzing home consumer behavior across thousands of real estate websites, one thing is becoming clear: borrower behavior begins forming much earlier than most lenders ever see, which is to say well before rates, pre-approvals, or lender comparisons enter the picture.

The lenders that stand out won’t be the ones competing hardest on price, but the ones that show up earlier with insight and guidance that align with how borrowers actually make decisions.

Borrowers don’t wake up one day ready to compare APRs. Long before they speak to a lender, they’re asking quieter, but more consequential, questions:

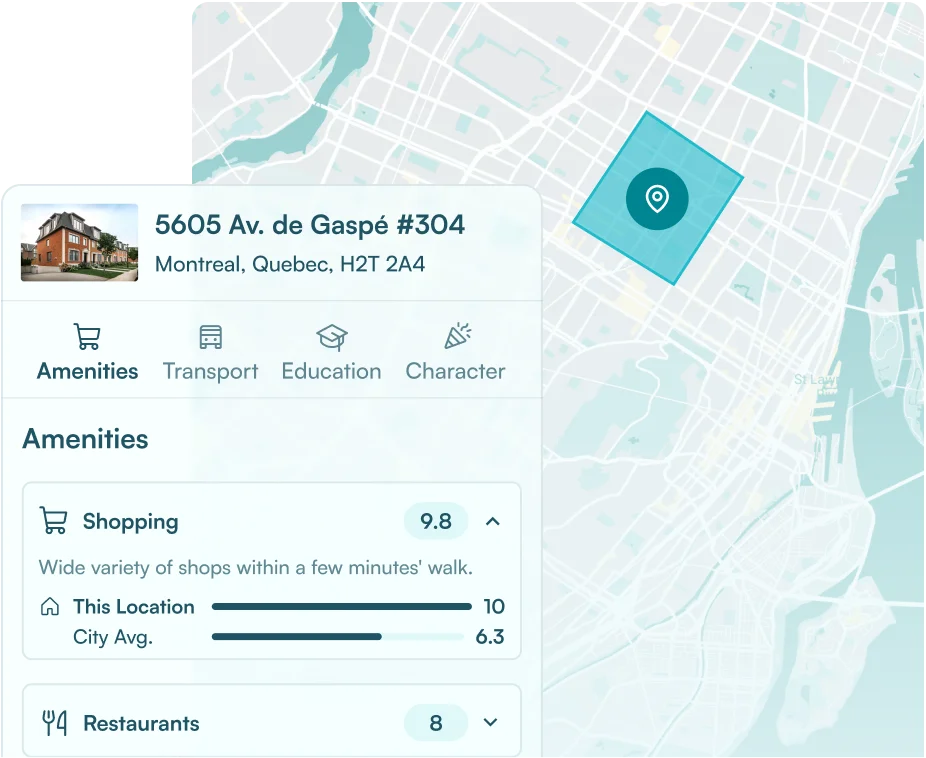

Those questions are answered while borrowers browse listings and explore neighborhoods, using signals like schools, transit access, walkability, and commute times to get an idea of what’s possible.

In that early phase, we consistently see borrowers:

By the time rate shopping begins, much of the emotional and directional decision-making has already taken place.

Examining home consumers’ engagement patterns from 2025 provides a clear view into what’s shaping borrower confidence early on.

As borrowers research where they might live next, the neighborhood insights they engage with most are:

These aren’t surface-level preferences. They directly influence how borrowers evaluate whether a move is viable. This shapes their perception of affordability, lifestyle fit, risk, and long-term stability, long before financing is even discussed.

At this stage, neighborhood context acts as an early decision filter, helping borrowers build confidence to move forward or rule out options. And by the time those signals are clear, the direction of intent is often already set.

Most mortgage companies only engage borrowers once these decisions have already started to form, which leads to the following challenges:

But with early behavioral insight, mortgage teams can understand:

That understanding is what makes the difference between simply reacting to borrower demand and shaping it earlier in the journey.

Mortgage teams that engage earlier in the journey are moving beyond transactional competition and into a role of trusted guidance.

By using early behavioral insight, they can:

Instead of leading with rates, these lenders help borrowers make sense of the move itself, building trust and relevance before price becomes the primary differentiator.

The most forward-looking mortgage teams don’t try to replace agents or listing platforms. Instead, they focus on building borrower confidence alongside them. They:

As a result, when financing conversations finally begin, these lenders aren’t just one of many options. They’re already familiar, credible, and aligned with the borrower’s goals.

The biggest shift isn’t a change in what borrowers want, but when their decisions start to form. Intent, hesitation, and confidence are taking shape as borrowers browse listings, explore neighborhoods, and test what feels possible, which happens long before they ever compare rates or contact a lender.

Mortgage companies that learn to engage at that stage aren’t just improving conversion later in the funnel. They’re changing when the relationship begins, and building trust before price becomes the deciding factor.

Want to see what early borrower behavior looks like in your market?

We’re happy to share what we’re seeing across thousands of real estate websites and how mortgage teams are using early insight to engage borrowers sooner.

👉 Book a time to talk with our team