Explorer par

Cas d'utilisation

Industries

APIs

Produits

Aidez les consommateurs à trouver la propriété parfaite en fonction de leurs préférences de style de vie.

Augmentez l'engagement des utilisateurs et améliorez la visibilité des annonces immobilières grâce à des données locales dynamiques.

Améliorez les classements SEO en positionnant votre marque comme la source de référence pour la connaissance des quartiers.

Donnez à vos agents des données de localisation uniques pour améliorer leur performance, attirer de nouveaux talents et augmenter la rétention.

Stimulez l'engagement des consommateurs grâce à des données géographiques intuitives.

Exploitez des données intuitives pour améliorer la qualité des prospects et la satisfaction des membres.

Améliorez la satisfaction des clients et augmentez les ventes avec des données géographiques exploitables.

Renforcez votre plateforme avec des données géographiques précises et flexibles.

Accédez à des données démographiques détaillées pour les quartiers ou des emplacements spécifiques.

Obtenez des scores de localisation puissants pour les quartiers et des adresses spécifiques.

Accédez à des profils de quartier détaillés qui enrichissent votre projet avec du contenu riche et lisible.

Tirez parti de données détaillées sur les points d'intérêt pour enrichir votre projet avec des insights géographiques complets.

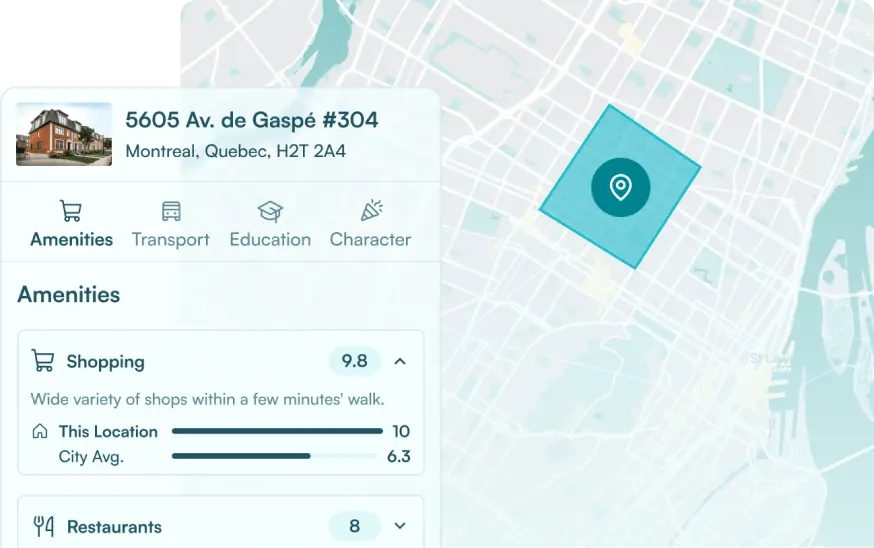

Obtenez une vue complète de n'importe quel emplacement avec des informations détaillées sur les points d'intérêt, les scores, les données démographiques, et bien plus encore.

Accédez à des statistiques et des données de marché détaillées pour tout quartier.

Découvrez les caractéristiques de localisation clés qui font augmenter ou diminuer les valeurs immobilières.

Améliorez vos offres immobilières avec des données scolaires détaillées et personnalisables.

Évaluez l'impact du changement climatique sur les propriétés avec des scores de risque climatique complets.

Caractéristiques de style de vie et de localisation que les consommateurs recherchent.

Analyses démographiques complètes et intuitives.

Outil de recherche basé sur le style de vie pour aider les consommateurs à trouver l'accord parfait.

Accédez aux rapports de localisation les plus robustes de l'industrie.

Montrez votre expertise locale et augmentez le trafic organique avec des pages de quartier prêtes à l'emploi.

22 Avr 2024

Insights

| 15 Août 2024

Partnerships

| 24 Juil 2024

| 12 Juil 2024